Federal Government Action Will Assist Renters in Maintaining Income; Strong Multifamily Fundamentals Pre-Coronavirus Provide Sturdy Framework

Unemployment benefit expansion mitigates financial impact. Many throughout the nation are faced with uncertainty as COVID-19 rattles the economy and labor markets. The federal government has been fast-acting in its response, exhausting numerous fiscal and monetary measures to keep the economy afloat and provide income to those who suddenly face hardships. Unemployment benefits have been both increased and expanded, supporting laid-off workers’ ability to stay up to date on important bills, including rent. The new criteria for unemployment benefits include freelance workers, the self-employed, contractors, and part-time personnel in addition to those who would typically meet specified standards. The federal benefit period lasts until July 31, and those who qualify for unemployment will receive $600 per week on top of a state benefit, which varies throughout the nation and generally aligns with the cost of living. State benefits will also be extended an additional 13 weeks beyond the exhaustion of the prototypical benefit period. This action will be wide-reaching and relieve some of the stress that hangs over both tenants and owners of multifamily. Although, the process of distributing payments will likely be delayed as unemployment offices are being overwhelmed with requests.

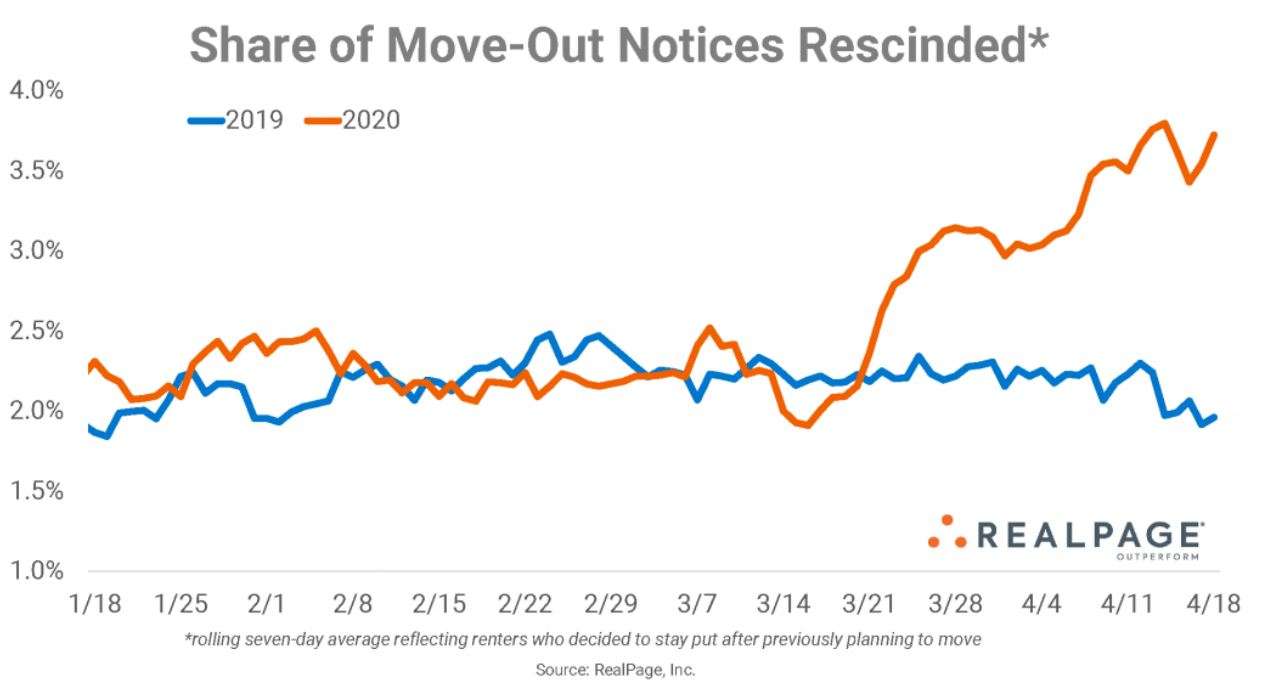

Government payment provides renters with an income stream to offset financial burdens. The other vital aspect of the stimulus package is the one-time payment to all adult Americans that filed taxes in 2018. Most adults will receive $1,200 in addition to $500 per child under the age of 17, with installments phasing out for individuals that made over $75,000 and dropping off completely above the $99,000 threshold. The federal government has indicated that direct deposit payments will arrive by the end of April; however, those who will be receiving checks in the mail might not get them for at least a couple of months. The additional income should make up for some wage losses and supplement income streams for those who have not been negatively impacted. Based on early reports, 69 percent of renters were able to meet April rent obligations by the fifth of the month, down 13 percent year-over-year despite unparalleled circumstances.

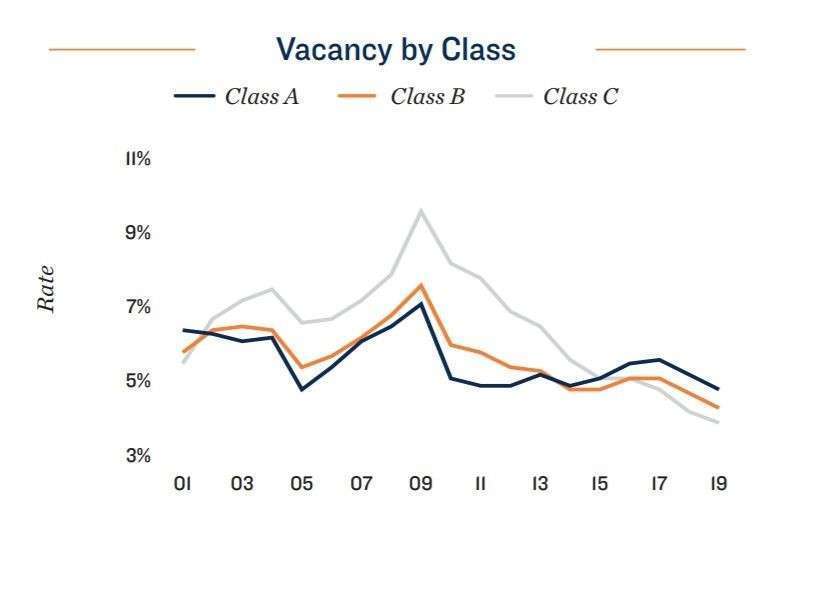

Apartment fundamentals on solid footing entering this year. Multifamily housing performed exceptionally well over the course of this cycle, driven by the affordability of renting an apartment relative to owning a single-family house, and the younger generations’ preference for leases and added amenities. Over the past few years, workforce rentals became increasingly undersupplied, as vacancy was near 20-year lows ending 2019. Among the three segments, Class C vacancy contracted by the greatest margin since 2009’s peak, dropping 570 basis points into the mid-3 percent range. Class B vacancy followed closely behind, dropping 330 basis points since the Great Recession peak into the low-4 percent area as of the beginning of this year. Tightening conditions have supported the need for rapid inventory growth; however, rising construction costs have led builders to construct more Class A units, which has not provided much relief for the budget-friendly rental segment. Despite the elevated construction of luxury apartments over the past decade, Class A vacancy has also dipped 230 basis points since 2009 into the 5 percent range, demonstrating robust demand throughout all echelons of multifamily housing.

Challenges Presented by the Virus-Driven Downturn

Will Differ Throughout the Nation

Some markets and niches are better prepared to weather the storm. The risk level that the apartment industry will face differs throughout the country, as some markets and population segments will have to combat more pronounced headwinds. Lower-tier space may be burdened by the fact that their tenant base is more likely to be affected by job losses and financial hardship, whereas midtier space might be better suited to maintain cash flow. Additionally, upper-tier space has a stronger ability to avoid losses from missed rental payments as more tenants are able to work from home and have savings built up; however, newly built luxury apartments will find it difficult to build a tenant roster over the short term. Working-class rentals in some of the nation’s more expensive cities will face obstacles as government payments don’t go as far as to cover monthly rental costs. On the other hand, metros with diverse economies will be less at risk as several sectors of the U.S. economy are still functioning, including technology, industrial and construction.

Multifamily owners will have to overcome hurdles. In the short term, finances will have to be closely watched and managed, as a reduction in rental income is entirely possible, while expenses may arise concurrently. The extra costs to maintain clean common areas through increased labor and sanitation, as well as the likelihood of more maintenance expenses linked to wear and tear as residents spend more time than usual in their apartments will be hurdles. Additionally, owners of newly built apartments will find it more difficult to fill units, as fewer people are moving around and actively searching for residences. A longer-term headwind could be the slowdown of household creation amid more people moving back in with their families or seeking roommates due to financial burdens. These challenges will dissolve once the economy is returned to full functionality and the health crisis is over, but with no clear timetable, it is important for owners to be cognizant of the obstacles they will face.

National Insights:

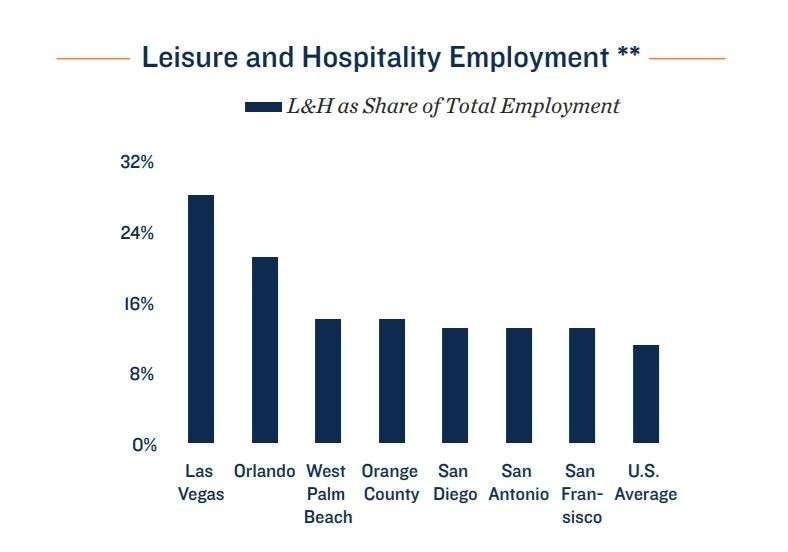

• Large tourism-based economies are facing more direct impacts that will weigh on their labor force. These headwinds may linger until the population feels safe traveling again.

• Rentals in markets at the height of their COVID-19 outbreaks are more at risk from strict shelter-in-place orders. State and local government reaction will be vital to regaining economic momentum.

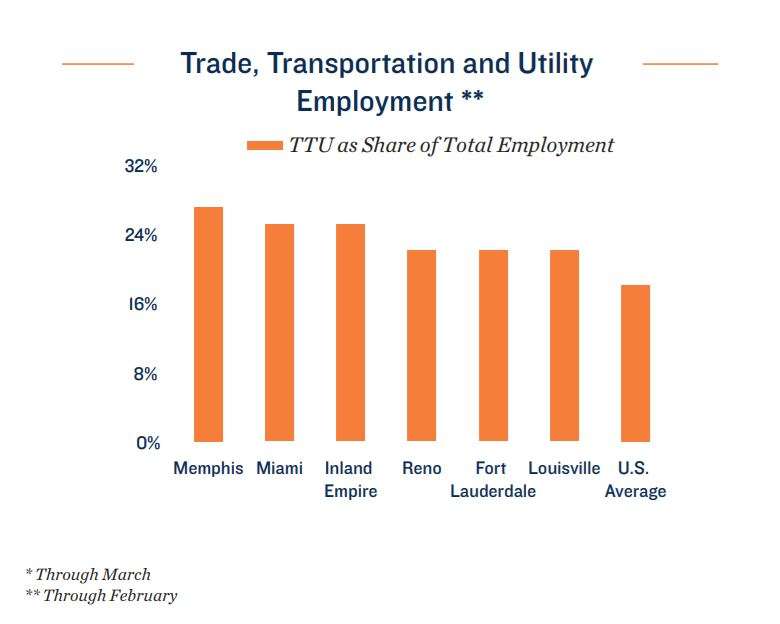

• Regional logistics hubs in the Midwest and the central U.S. may be more stable, as e-commerce will act as a tailwind in maintaining the job market. Although, international supply-chain disruptions may have an adverse impact on some coastal markets.

Federal agencies and local governments putting moratoriums on evictions. The CARES Act initiated a 120-day eviction moratorium that disallows borrowers of federally backed mortgages or who participate in federal assistance programs from beginning eviction proceedings for nonpayment, started on March 27. These same landlords must also give tenants a 30-day notice to vacate the property after the eviction moratorium period has passed as well as conform to local eviction laws. Landlords that fit into these classifications and have fewer than five units fall under the homeowner protections included in the CARES Act, which disallow evictions for 60 days started on March 18. Properties without federally backed mortgages or that do not participate in federal assistance programs would default to the state provisions. More than half of the state governments have enforced a pause on evictions, typically lasting between 30 and 60 days. Additionally, local governments, particularly in some of the nation’s most densely populated cities, have followed suit in halting evictions through at least the end of April. Owners that are not disallowed from evicting tenants should take into consideration that it may be more challenging to fill vacant units given the current conditions.

National Multifamily Housing Council Recommendations:

• Halt evictions for 90 days for those who can show they have been financially impacted by the COVID-19 pandemic. (Does not apply to evictions for other lease violations such as property damage, criminal activity or endangering the safety of other residents and staff .)

• Avoid rent increases for 90 days to help residents weather the crisis. Create payment plans for residents who are unable to pay their rent and waive late fees for those residents.

• Identify governmental and community resources to help residents secure food, financial assistance, and healthcare and share that information with residents.

Borrowers of federally backed mortgages granted relief. The Coronavirus Aid, Relief, and Economic Security Act includes protections for those with multifamily mortgages backed through federal agencies, including Freddie Mac and Fannie Mae. Borrowers of these agencies may request loan forbearance, given that they were on time with payments through February 1 and can provide proof of financial hardship from the new coronavirus. The period of forbearance is initially set at 30 days, with two additional extensions available for borrowers that request it within the time frame specified in the agreement. This may be a resource that provides owners an opportunity to cushion themselves, while being aware that it includes stipulations for owners, including bans on evictions and disallowing late payment fees. Additionally, those who seek forbearance will be required to repay within 12 months. Borrowers with mortgages through private lenders should communicate with their providers to discuss options that are available to help them through this challenging time.

Governments Pausing Evictions;

Loan Forbearance Available for Borrowers

Owners Acclimate to Changing

Conditions; Long-Term Outlook Strong

The apartment industry is adapting to combat headwinds. During times of uncertainty, owners may find it necessary and beneficial to be more hands-on with their investments. Open communication with tenants regarding their financial status could formulate realistic expectations for rental income so that owners can anticipate any losses and put plans in place to maintain cash flow. Additionally, owners facing financial uncertainty should reach out to lenders to discuss loan forbearance options and talk to property managers about logistics and operational procedures. Every owner will face their own unique challenges, and the ability to adapt while in the unchartered territory of a global pandemic will be favorable in prospering through these headwinds. Some may even find this is an opportunity to retain quality tenants through new leases, as they are less likely to explore other options during the crisis. Investors looking to buy and sell will have to discover new pricing as the eminent downturn will alter asset values and underwriting standards.

Multifamily remains a solid commercial real estate investment through periods of uncertainty. The $2.2 trillion stimulus bill provides a safety net for the short term while the population works together to slow the spread and medical researchers race to find a vaccine that can bring a sense of normalcy back to daily life. Multifamily owners are concerned with the financial impact that will come of this, but several factors support an optimistic viewpoint. Government payments and unemployment benefits will help renters replace lost income over the near term, enabling them to pay on time. The underlying trends that have supported apartments throughout this cycle continue to be in place and will sustain robust demand for rentals in the long term. One of the fundamental principles driving multifamily housing is that people will always need a place to live. The global pandemic will not push prospective renters toward single-family housing as an alternative as the rent to home payment gap remains significant.

National Multi-Housing Group

John Sebree First Vice President, National Director | National Multi-Housing Group

Prepared and edited by

Ben Kunde Research Associate | Research Services

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guaranty, express or implied, may be made as to the accuracy or reliability of the information contained herein. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Experian; Federal Reserve; Global Financial Data; MBA; Moody’s Analytics; NYSE; Real Capital Analytics; RealPage, Inc.; Standard & Poor’s; TWR/Dodge Pipeline; U.S. Census Bureau; Yardi © Marcus & Millichap 2020

Randolph is a Multifamily Investment Sales Broker with eXp Commercial servicing Multifamily Buyers and Sellers in the Greater Chicago Area.